“Covid-19” Impact on Cryptocurrencies and Blockchain

Viktor Fischer — Managing Partner Rockaway Blockchain Fund

What happened?

Protective measures against the coronavirus, such as containment and social distancing, are having direct impact on the economy. Fitch Ratings now projects the world GDP to decline -1.9% while Bloomberg expects the US unemployment rate to exceed 20%. By mid-March, indexes fell by 30% globally from their peak this year, as investors priced-in reduced future profits. Even gold, once considered a safe haven, dropped initially by 11% as investors needed liquidity to cover margin calls and losses. When assets’ prices fall, fear of uncertainty causes investors to shift capital to safe assets. For instance, inflow of capital into 10-year US treasury bonds reduced their yield from 1.9% at the beginning of this year to 0.8% (lowest in history). As of mid-April, significant monetary and fiscal policies helped the markets to recover half of the decline, at least temporarily.

Fear of uncertainty and flight from risky to safe assets has also had an effect on cryptocurrencies, but even to a greater degree. Bitcoin price declined 50% from $10.000 on February 14 to $5.000 on March 17. Initially, Bitcoin price declined in-line with the decline of traditional markets (see point A on the chart below). On March 12 and 13, the continued sell-out of investors was accentuated by 3 strong shorts manipulating the price of Bitcoin on BitMEX — the largest exchange for bitcoin futures. The decline caused liquidations of traders, who got long squeezed. Solely on BitMEX, liquidations that followed in the next 24h amounted to $1.3bn. In addition, BitMEX suffered a DDoS attack, which caused it to shut down its system in order to stop losing its insurance funds and causing a price difference compared to other exchanges (see point B on the chart below).

The overall decline was caused mainly by the sell-off from short-term investors, who held bitcoin for 6 months or less4. Bitcoin represents ~60% of the market capitalization of all cryptocurrencies, with which it is highly correlated. The decline in Bitcoin caused a drop in the entire market, which decreased 54% from $300bn on February 14 to $140bn on March 16. As of mid-April however, both bitcoin and overall cryptocurrency market capitalization have returned to their January 2020 levels, while the traditional markets are still ~15% below their January levels. So rather than speculate on the price, let’s take a look at other implications of the Covid-19 situation.

What are the opportunities for cryptocurrencies and blockchain?

- Stablecoins: Investors shifted their capital into safe assets, called stable-coins (tokenized USD). Stablecoins’ supply now reaches $9bn, dominated by USDT (Tether), while their transaction volume is now nearly as high as bitcoin transaction volume.

Chart: Stablecoin supply

There are 3 main reasons for the growth of stablecoins:

-

Flight to safety from risky assets, as crypto investors were shifting their positions from volatile to stable assets

-

Growing demand in emerging economies for USD, as their local currency was weakening against the dollar. It is simple to buy USDT on Kraken from practically anywhere

-

Digital payments and remittances, as physical cash payments became impractical in the reality related to coronavirus (e.g. travel bans, lockdowns).

We expect an increase in usage of stablecoins, particularly in the fields of digital payments and cross-border remittances. For instance, US government Covid-19 stimulus includes a payment of $1200 directly to natural persons, but 8% of the population is unbanked and 30% of the population hit zero balance triggering overdraft fees. Companies such as Celo.org are working on a solution for digital cash. If you want to try sending digital money fast and cheap to a friend living overseas, download Argent wallet and use DAI stablecoin.

- Trading: Daily trading volume of cryptocurrencies on the spot market has been steadily growing 300% year over year since 2015 and is up 185% since the beginning of the year, reaching $120bn per day, 3x as much as during the 2018 crypto boom market.

Earlier this month, Binance (#1 spot exchange) acquired Coinmarketcap.com, reportedly for $400m8, likely in order to control its acquisition channel. With 37m monthly visitors, Coinmarketcap is the most visited website in the crypto space, and the largest referrer for all exchanges.

In the derivatives market, the trading volume is $10bn per day on futures and $50m on options skew.com, a decline of 50% from its peak, but slowly getting back to previous highs.

We expect the high volatility of this asset class btcvol.info to drive further increase in trading volume, especially in options, which are used by professional traders to trade volatility and by institutions to hedge their positions against further declines. This will increase revenues of derivatives exchanges such as Deribit, BitMEX and FTX.

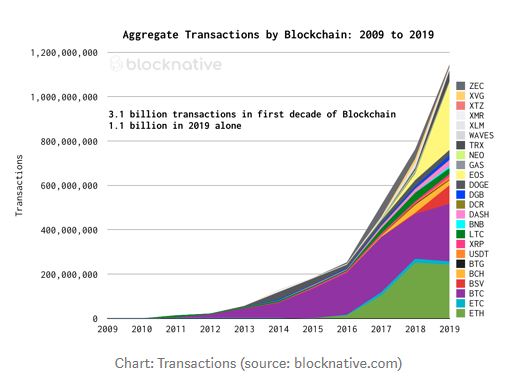

- Usage: Transactions on blockchains have been growing at 44% CAGR, reaching 1bn transactions in 2019. Nearly half of the transactions are executed on Bitcoin and Ethereum.

On Ethereum particularly, the growth in transactions often resulted in congestion of the network, which runs at 80% utilization on average. This was also the case mid-March, when Ethereum network congested, causing issues in other projects running on Ethereum (e.g. MakerDAO). We expect teams to accelerate finalization of their scalability solutions for Ethereum, or faster alternative programmable blockchains, such as Solana.com, which launched its mainnet on March 16 (Disclaimer: Solana is a portfolio company of Rockaway Blockchain Fund).

- Financial services: Unprecedented monetary and fiscal policy resulting from the Covid-19 financial measures will pump trillions of dollars into the economies. Interest rates are ranging from negative (-0.75% in Switzerland) to zero (0% in Euro zone, 0.25% in US). Quantitative easing and asset purchases by central banks is set to “unlimited”, with central banks buying not only government bonds, but also corporate bonds (and considering equity). Monetary base (M2 of 12 major economies), which already doubled from $40tn to $80tn since 2008 financial crisis, will continue to increase, potentially driving hyperinflation and decreasing relative value of cash10. Prices of assets will increase, and it will be difficult to find yield. On the other hand, small and medium enterprises will have difficulties getting loans, due to worsened economic conditions, and the credit spreads will increase.

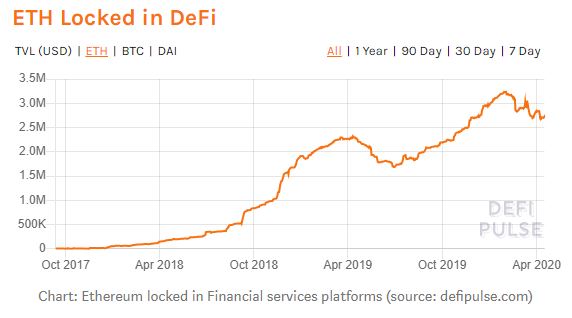

Financial services on blockchain are called DeFi (“decentralized finance”). They allow participants to lend, borrow, pay, invest and generate yield without passing through the traditional financial system. DeFi services include:

-

Lending and borrowing platforms such as Compound.finance or Nexo.io, where you can lend money to someone else, who uses cryptocurrency as collateral, thus reducing counterparty risk. Current yields are around 8% p.a. on Nexo

-

Liquidity pools, such as Uniswap, which let you participate on a decentralized exchange, earning money from trading fees (but also being exposed to trading loss). Uniswap pool has generated 2.4% yield since mid-March

-

Structured finance platforms, such as Tokensets.com, where you can invest into structured products, which automatically rebalance your position. For example, a set on Tokensets called ETH 20 day MACO yield set has generated 15% yield since mid-March

Ethereum locked in these platforms has been increasing since 2017 and is now hovering at around 3m (~$500m), where it seems to have stabilized. Market decline in mid-March has stress-tested these platforms, which are now implementing their learnings to ensure robustness (e.g. scalability, automatic stop-loss or circuit breakers, reliable price feeds via oracles and simplified user interfaces).

In the world of high volatility, we expect to see increased usage of lending platforms (e.g. by traders for leverage and by miners for saving keeping future upside from the mined block rewards), borrowing platforms (e.g. by traditional businesses tokenizing their revenue streams such as music artists on Spotify) and increased demand for decentralized insurance (e.g. to insure deposits). We expect financial services to be the main driver of incoming capital into cryptoassets (to use MakerDAO or Compound, one has to buy DAI stablecoin with Fiat money).

If you want to try some of these services, go to Loanscan.io for the list of yield on lending platforms, Pools.fyi for the list of liquidity pools. For an easy to use interface, we recommend to use the “decentralized bank” application Zerion.io. Zerion has written a blog post on how to generate yield in DeFi, based on data from Q1 2020.

- Data: Lack of consistent and verified data has been a critical issue in fighting the Covid-19 crisis (not only in the number of infections, but also in the virus-related data and patient-related data). IBM Hyperledger has been supporting MiPasa.org project to reconcile, validate and share data in a public health context. MiPasa gathers, combines and validates data from CDCP, WHO, Israeli Ministry of Health, John Hopkins University and others. A real benefit of blockchain is that it provides trustworthy data by verifying the source via public/private signatures and helps different administrators to collaborate over the validity of data11. MiPasa then enables sharing of the information in a private manner, among government agencies, health institutions, research centers, hospitals, retirement houses and the public to orient research, prevention and recovery efforts.

Conclusion

The drop in cryptocurrency prices can be mainly attributed to fear and speculation, rather than to a change in fundamentals. We see continued growth in stablecoins, trading volume, transactions, financial services and data sharing implementations of blockchain technology. Given the digitally native form of the industry, blockchain-based financial services do not suffer from implications of the epidemics as much as traditional banks do. Decentralized services (such as lending / borrowing platforms, payments, decentralized exchanges) are fully automated and run by computers regardless of whether people are constrained by a lockdown or engaged in economic activity.

About the Author

Viktor Fischer is the managing partner of Rockaway Blockchain Fund. Prior to Rockaway, Viktor worked as Junior Partner at McKinsey & Company, focusing on M&A and corporate finance. Prior to McKinsey, Viktor co-founded Innovatrics, a start-up focused on biometric identification, which won multiple awards, such as Deloitte Top 50. As a hobby, Viktor has been teaching corporate finance and valuations at Charles University in Prague, University Paris XI, and accelerators such as StartupYard, Wayra in Prague and The Spot in Slovakia. Viktor holds a Masters Degree from HEC Paris and MBA from INSEAD.

APPENDIX: Sources of data

-

bloomberg.com/news/articles/2020-04-14/worst-case-fears-of-20-30-u-s-jobless-rate-are-now-realistic

-

blog.bitmex.com/how-we-are-responding-to-last-weeks-ddos-attacks

-

coinmetrics.substack.com/p/coin-metrics-state-of-the-network-30a

-

coindesk.com/usd-stablecoins-are-surging-but-zero-interest-rates-complicate-business-model

-

nasdaq.com/articles/why-covid-19-stimulus-should-incorporate-digital-dollars-2020-03-25

-

coindesk.com/binances-coinmarketcap-acquisition-is-a-bet-that-crypto-really-is-for-the-masses

-

cointelegraph.com/news/blockchain-provides-trusted-data-to-counter-spread-of-coronavirus