The Tokenization of Assets

By Jakob Roth, Fabian Schär and Aljoscha Schöpfer - Center for Innovative Finance, University of Basel

Public Blockchains allow the transfer of digital assets in a truly peer-to-peer manner. However, the assets that can be represented on a Blockchain natively are limited to assets that are created as part of the protocol, such as Bitcoins in the case of the Bitcoin Blockchain. Any asset that originates outside the Blockchain can only be traded on-chain if it gets a reliable on-chain representation. This representation is usually referred to as a token. In short: Tokens are rivalrous, digital units of value that entitle the owner to an asset or a utility.

In this text, we present three categories of tokens used on public Blockchains, namely UTXO-based, layer-based and smart contract-based tokens. This will provide the reader with a short overview of the history and the current state of tokenization.

The first category of token standards to emerge is usually referred to as UTXO-based, or Colored Coins. This token type is created by using a native Blockchain asset (or more precisely an unspent transaction output), e.g. a fraction of a Bitcoin, and attaching an external promise to it. In more technical terms, colored coins are created through a genesis transaction, which uses an additional output to add metadata to the transaction graph. Compatible wallets will thereafter treat the corresponding outputs separately from any other Bitcoin unit, making them non-fungible.

To use an analogy, one can think of a five-dollar bill on which someone writes a promise to deliver an ounce of gold. The five-dollar bill could freely circulate — including the attached promise. Similarly, any asset (promise) could be attached to a Bitcoin fraction and transferred on-chain, which could lead to potential efficiency gains.

However, one major drawback of this token standard is the fact that the tokens can be lost rather easily, because the wallets are required to recognize colored coins. If they do not (this is the case for most wallets), they will treat the colored UTXO like any other UTXO and use it for ordinary Bitcoin transactions.

The second major category refers to layer-based tokens. Similar to the previous category, tokens are also created by using transaction outputs. But in contrast to Colored Coins, these outputs are generated through OP_RETURN transactions. This opcode allows anyone to add arbitrary data to the Blockchain. However, Bitcoin-like Blockchains cannot interpret this data natively. It is therefore necessary to create a corresponding transaction graph that keeps track of this data on a second layer. This second layer also allows for more features, including additional consensus rules, transaction types and requirements. At the same time, the base layer can provide a certain degree of security by anchoring transactional data in the original Blockchain.

To employ another analogy, consider a (hypothetical) transaction system based on text that is printed in the public advertisement section of a newspaper. A person intending to transfer an external promise to someone would publish this transaction message in a codified and compressed manner in the newspaper (representing the underlying Blockchain). An external system (transaction graph) would then interpret the information from the newspaper and include the corresponding transfer in its transaction system. This creates a system for the exchange of value which benefits from the properties of the first layer (e.g. public verifiability).

The third category refers to smart contract-based tokens. As suggested by the name, these standards use smart contracts to create and track states that represent token ownership. In particular, they map tokens to current owner addresses. Whenever someone wants to transfer a token, this person needs to interact with the contract and make a corresponding transfer call. If successful, i.e. if a person can provide cryptographic proof of ownership, the state of the contract is adjusted accordingly.

The vast majority of smart contract-based tokens are built on Ethereum’s ERC-20 token standard. This standard defines a set of rules that the tokens have to comply with, for instance how tokens can be accessed and transferred. By August 2019, there were more than 220,000 ERC-20 compatible token contracts on the Ethereum mainnet, over 1,100 of which were listed on exchanges. However, ERC-20 also has certain drawbacks. In particular, token interactions with (smart) contract accounts require two function calls. If a person accidentally calls the wrong function, the funds may end up stuck in the receiver contract. This is a severe problem and many ERC-20 based cryptoassets have been lost that way. ERC-223 and ERC-777 are alternative standards based on Ethereum, which mitigate the problem of lost tokens by allowing tokens to always be sent with the same function. However, none of the alternatives seems to gain traction and ERC-20 so far has remained to be the dominant standard.

In addition to the previous token standards, smart contract-based tokens can also be used for non-fungible assets such as collectibles. For these kinds of assets, the dominant standard is ERC-721.

Regardless of the many advantages that tokenization can bring, it is important to keep in mind that tokenization per se does not solve the counterparty issuer risk. This means that even if one owns a token, it does not guarantee that the external value is actually in issuer’s possession. A potential trading partner could still simply not deliver the external asset. An exception of this are native digital assets (e.g. Cryptokitties) or promises based on custodial smart contracts that lock the underlying assets (see DAI).

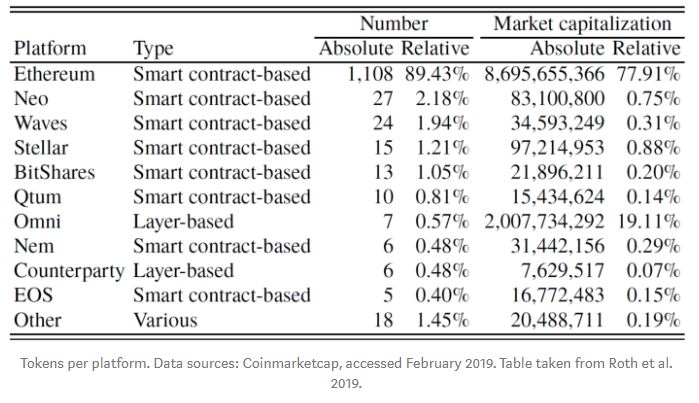

Let us conclude by looking at the following table, which provides an overview over the different token standards and their popularity. As can be seen in the table, smart contract-based token standards dominate the field in both number of exchange listed tokens and their respective aggregated market capitalization. Most of these tokens are built on Ethereum. For layer-based token standards, the case is likewise clear. Omni (formerly Mastercoin) is the leading platform in terms of market capitalization, thanks to the relatively high volumes of its variant of the Tether stablecoin. Other prominent examples of layer-based tokens include Bitcrystals (Counterparty) and MaidSafeCoin (Omni). Because UTXO-based tokens have almost completely fallen into oblivion, they have not been included in the table.

This text summarizes parts of Roth, Schär and Schöpfer (2019) which is covering the applications of tokenization in equity-crowdfunding. Download the working paper here.