Scenarios that might get spot Bitcoin ETF approved in the US

The views and opinions expressed in this op-ed article are those of the authors and do not reflect any position by Copper.

Once again, the US Securities and Exchange Commission denied a spot Bitcoin Exchange Traded Fund. Crypto crowds, angry and perplexed vow to fight another day. The answer however might be fairly obvious. But the options to get approval could unravel the core ethos of decentralization if key industry players comply with what is likely being implied and not being said.

The crypto community’s overzealous focus on getting a spot Bitcoin ETF approved has given the SEC a great amount of leverage. The regulator holds a very strong hand and it’s not about to fold without winning some if not all the chips. They’ve certainly understood how much cryptocurrency adopters would rejoice in a spot Bitcoin ETF approval as a mark of pride akin to divine affirmation.

Since 2017, and along with every denial of an ETF, the watchdog has continued to state that the cryptocurrency trading industry has yet to establish “comprehensive surveillance-sharing agreements with a regulated market of significant size” (see 2020 Copper In-Depth report).

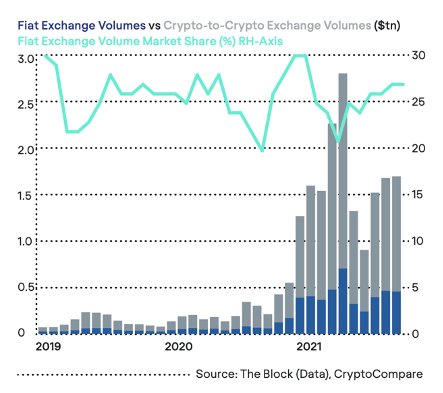

Many will argue that CME futures and US-based exchange volumes are now in the trillions annually. Fair enough.

However, all combined, this would still account for a fraction of the global market, most of which is happening on unregulated exchanges that the SEC has little power and reach over.

What the SEC might really be saying is that US-based and other regulated exchanges have too little a market share of the total trading volume of a global asset class. And they’re not wrong. Fiat-to-crypto exchange volume shows that they’ve cornered a tad over 25% of the market with little sign of gaining any additional share against their competitor crypto-to-crypto exchanges (see chart).

Which leaves the crypto industry with only a few solutions that would get the SEC to approve a spot Bitcoin ETF.

The first scenario, and most tedious, is that regulated exchanges become the aforementioned ‘significant-size’. This would be slow and have little guarantees of ever actually happening considering the size of the competition.

More dangerously and under the banner of self-regulation, US-based exchanges can opt to ban incoming Bitcoin and other cryptoassets from unregulated exchanges.

The latter option would be akin to an attack on Bitcoin of epic proportions breaking the cryptocurrency’s parity from within. Famed cryptocurrency educator Andreas Antonopoulos said in an interview that “tainted coins are very destructive. If you break fungibility and privacy, you break the currency. If [fungibility] is not fixed, it is possible to attack Bitcoin in ways we haven’t seen yet and that could prove very effective.”

On the one hand, such an exercise would be a fairly simple task for regulated exchanges to execute. Contrary to many government and financial bodies who continue to harp on about money- laundering, the blockchain is transparent and tools plentiful to address this particular issue.

The result, however, would bring a parallel market with Bitcoin becoming an unattractive asset to transact with. Exchanges, regulated or otherwise, understand well that such a policy would be fairly destructive for the industry they cater to. As such, it’s unlikely to be a viable option as it would not only bring the competition down, but themselves along with it.

It would also spell doom for the competitive advantage that the US currently basks in. This is a scenario even the SEC would probably like to avoid being burdened with.

Win some, lose some

There is one more scenario that could prove powerful and effective with only short-term market effects. Regulated exchanges can amp up clearing requirements and add inbound limits from unregulated exchanges. Much like unregulated exchanges who have thresholds for not requiring Know-Your- Client (KYC), the opposite can be true for regulated exchanges whereby increased documentation and longer account-credit times can be placed.

This would increase compliance and at the same time significantly maim the allure of unregulated exchanges. While regulated exchanges were slow off the mark to add tokens in 2017 that propelled unregulated exchanges to new heights, this is no longer really the case. Regulated exchanges can and are catering to the crowds. This, in turn, would increase the market share of regulated exchanges and a ‘crypto-run’ would likely ensue on the mere mention of additional requirements which would border on sanctions.

Although this might seem as anti-competitive practice, it’s unlikely to upset regulators, if under the banner of self-regulation.

Is it worth it?

On the one hand, a Bitcoin ETF would likely reduce volatility as sell pressures would decline by the addition of longer-term investors. And lower volatility would further increase investor appetite.

But for that to happen, should this assessment be correct, crypto companies would have to effectively grey-list inbound Bitcoin from unregulated exchanges with a short-term risk of possibly ushering in a new era of double pricing.

On the other, a Bitcoin ETF approval would likely require that cryptocurrency operatives fold into greater self-imposed oversight, which would be a complete anathema.

He who blinks, loses?

Industry players can also wait it out. It might even be the better option for the cryptocurrency industry in the long-run. With no easy onboarding such as an ETF, investors might very well take their time to actually learn and participate in the ecosystem further cementing the digital asset’s footprint in the financial world. At the growth rates seen over the past two years, this would be a feasible scenario.

Yes, an ETF would increase demand. But the juice might not be worth the squeeze. The demand in all likelihood will come with or without it.

About the Author

Article authored by Fadi Aboualfa, Head of Research at Copper