Why it is wrong to say “Bitcoin prices correlate with global equities” and two other fundamental reasons for a strong Bitcoin

Authors: Prof. Dr. Philipp Sandner, Maximilian Bruckner

Crypto assets experienced a month like no other in May 2022. The collapse of the Terra ecosystem had a significant impact as Bitcoin prices also dropped in the immediate aftermath. The crypto markets have not fully recovered since then, in part also due to the state of the global economy and politics. Nonetheless, we believe that Bitcoin’s fundamentals remain strong even through this bear market. If anything, this event showed the resilience of Bitcoin in comparison to other projects which experienced much heavier losses. In this article, we address the common objection to the high correlation between Bitcoin and equities and name two key reasons for a strong Bitcoin going forward.

There is no persistent high correlation between Bitcoin and global equities

Almost every time we teach a seminar or hold a presentation about crypto assets, there is always some variation of this question asked: “Is it true that, as an investor with a diversified portfolio, adding Bitcoin does nothing for my diversification due to its high correlation with stocks?”. Our answer is a resounding “no”. There are several misconceptions at play here that prompt this question in the first place. While it is true that a static analysis of Bitcoin and equities at a given time may show a moderate correlation, rolling correlations show that these correlations are in fact much lower and tend to fluctuate significantly. From some says of stocks and Bitcoin moving in synchrony, we should not infer a correlation. If correlation exists, it is just temporary, not persistent over a longer period of time.

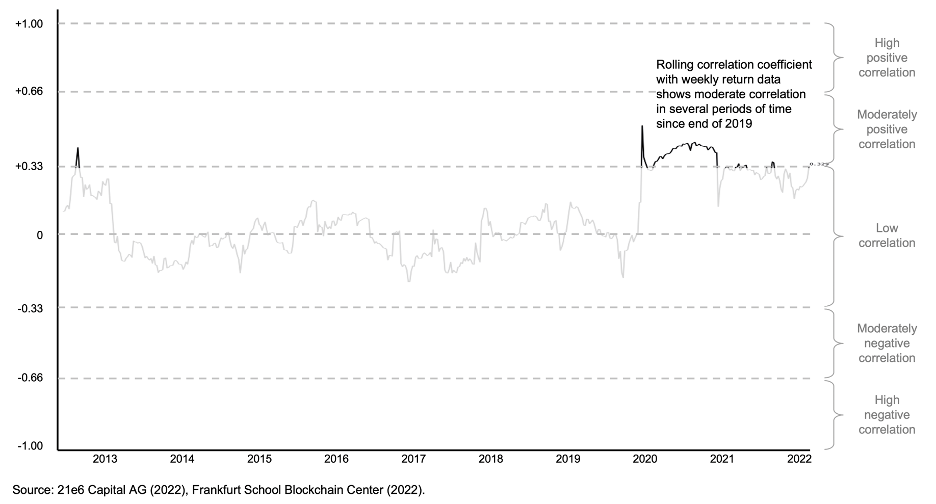

The right interpretation of the correlation is far from trivial. An analysis made by 21e6 Capital - as Swiss crypto advisor - shows weekly rolling correlations between Bitcoin and global equities (figure 1). Immediately, we can see a long period of fluctuations around the zero-correlation mark, right up until the corona crisis in March 2020.

Figure 1. Weekly rolling correlations between Bitcoin and MSCI World

(Source: 21e6 Capital AG, 2020; Frankfurt School Blockchain Center, 2022)

In March 2020, we observed an upward spike in correlation, up to a coefficient of 0.5 at its peak. At first glance (and in the context of the graph), this again seems like a high correlation. But this is also not quite correct: Generally, correlation coefficients between 0.3 and 0.7 indicate variables that have a moderate correlation. Statisticians only claim a “high” positive correlation at a coefficient above 0.7. So, even during periods of perceived elevated correlation, there is still really only a low to moderate correlation observed between Bitcoin and equities. The reason is that correlation is measured over a longer period of time.

To be fair, the fact that Bitcoin and equity correlations rise significantly in times of crisis does mean that crypto assets do not provide a good hedge against a crisis. However, recent financial crises also show that correlations between different asset classes in general increase significantly during a crisis. The reason is that all assets – from equities to gold, from other commodities to Bitcoin – react to harsh news like the COVID pandemic or the invasion of Ukraine. But longer term movements overlay such strong short term effects – yet, the latter are incorrectly perceived as “correlation”. Even gold (which often correlates negatively with the stock market) tends to display a short-term positive correlation to equities in those moments of crises. So, although crypto assets do not offer direct protection against negative market movements in times of crisis, one should by no means take from this article that crypto assets cannot add value at all. On the contrary, analyses show that the high risk-adjusted returns of crypto assets can significantly improve the characteristics of a portfolio [1]. Especially in the current environment, there are some fundamental reasons speaking for Bitcoin (and other crypto assets) which we will explore in the remainder of this article.

Bitcoin can be a hedge against inflation

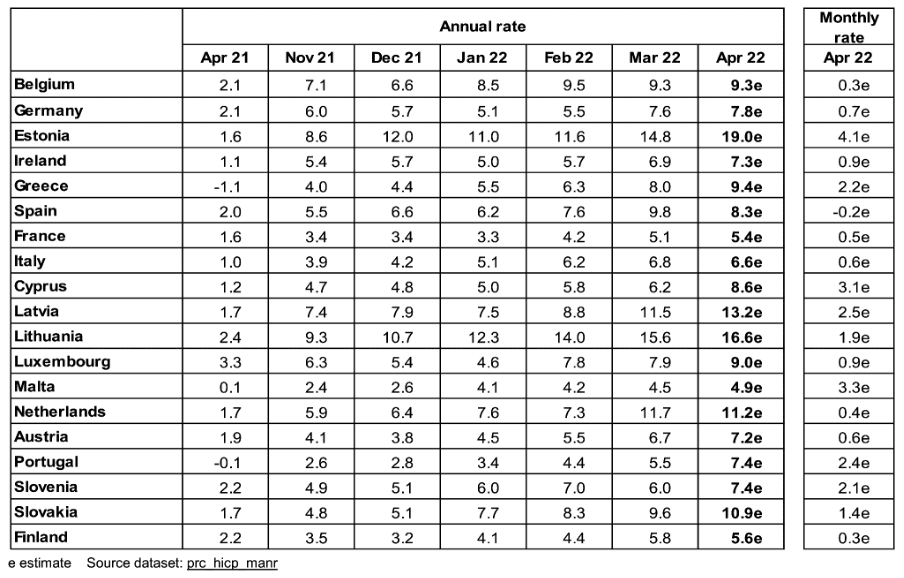

By the end of 2021, inflation had already risen to 5%. Now, only a few months later, inflation often clocks in at 7 to 8%. Figure 2 shows the latest estimates from the European Union's (EU) statistical office, Eurostat. In April 2022, they estimated the inflation rate in Germany at 7.8%. They also gave significantly higher estimates for other EU member states. Switzerland is sitting at around 2.5% annual inflation in April 2022 – better than its peers, but still rising significantly over time [2].

Figure 2: Inflation Rates (%) Measured by the HCIP in the EU (Source: Eurostat)

Bitcoin and similar crypto-assets offer a possible hedge against inflation, due to their underlying technical architecture. It is specified in the code not only how many new Bitcoins will be mined ("printed") per year, but also that there will never be more than 21 million Bitcoins in total. The code governing this is immutable due to blockchain technology. This is in stark contrast to the monetary policies of the world's central banks. But of course, this will only play out over the longer term. With “longer term”, we mean periods of multiple months or years.

Sanctions and confiscability

With Russian assets seized in the wake of far-reaching sanctions, it is evident that central bank assets are not absolutely safe. There is now a risk of confiscation/seizure of said assets. In the future, it will be part of central bank risk management to analyze the vulnerability of their reserve assets to sanctions or seizure in the months and years ahead. One attempt at a solution could be to buy gold or other commodities. However, this does not solve the confiscability issue. Talking about central banks and referring to the previous chapter on inflation, it also needs to be noted that central banks’ assets suffer of a currencies’ (expected) weaknesses: Some weeks ago, the central bank of Israel sold billions of US dollar and purchased Chinese currency.

Most of the world's assets are fundamentally vulnerable to confiscation. Foreign currency reserves, ships (like the oligarch’s yachts), real estate, gold, stocks, etc. are often not safe in this regard. But there is a new type of digital bearer asset which presents a remedy. Bitcoin, Ethereum, and to some degree stablecoins are inherently constructed in a manner that does not allow third parties to confiscate or seize them. Due to the private-key-public-key architecture (see Public-key cryptography), a standard component of blockchain technology, crypto assets are untouchable in this regard. But beware: this is only true if the assets are held on a so-called “cold wallet” (USB stick, pen writing on paper, or even simply in your brain) and not on a centralized exchange. The world is slowly beginning to understand that blockchain technology has birthed a new asset class that can technically never be taken against one’s will - by design.

It is only a matter of time…

In summary, we can see that Bitcoin holds a strong position amidst financial and geopolitical turmoil. Consumers begin to notice the effects of rising inflation firsthand. People also started looking for a safe asset that, unlike cash, generates positive returns. Recent events show that assets traditionally considered safe may very well be seized or otherwise lost. Large parts of the Russian Central Bank’s assets and oligarchs’ fortunes have been frozen. Many Ukrainians have also lost their assets as a result of the war – sometimes, the only thing they have left is their crypto assets. We believe that these factors will make a significant contribution to the further adoption of crypto assets and especially Bitcoin in the medium and long term.

References

[1] 21e6 Capital, 2022: What Happens To Your Portfolio When You Invest in Crypto?

[2] Swiss Federal Statistical Office, 2022

Remarks

This article is an informational document and does not constitute an investment recommendation, investment advice, legal, tax or accounting advice or an offer to sell or a solicitation to purchase any securities, crypto assets, or tokens, and therefore may not be relied upon in connection with any offer or sale of securities, crypto assets, or tokens. The views expressed in this letter are the subjective views of the authors, based on information which is believed to be reliable. Any expression of opinion (which may be subject to change without notice) is personal to the authors, and the authors make no guarantee of any sort regarding accuracy or completeness of any information or analysis supplied.

About the Authors

Prof. Dr. Philipp Sandner has founded the Frankfurt School Blockchain Center (FSBC). From 2018 to 2021, he was ranked among the “top 30” economists by the Frankfurter Allgemeine Zeitung (FAZ), a major newspaper in Germany. Further, he belonged to the “Top 40 under 40” — a ranking by the German business magazine Capital. He has been a member of the FinTech Council and the Digital Finance Forum of the Federal Ministry of Finance in Germany. He is also on the Board of Directors of FiveT Fintech Fund, 21e6 Capital and Blockchain Founders Group - companies active in venture capital financing for blockchain startups and crypto asset investment management. The expertise of Prof. Sandner includes blockchain technology in general, crypto assets such as Bitcoin and Ethereum, decentralized finance (DeFi), the digital euro, tokenization of assets and digital identity.

Maximilian Bruckner is Head of Marketing & Sales at 21e6 Capital AG. Prior to this, he was engaged as Executive Director of the International Token Standardization Association (ITSA) where he focused on research and classification of crypto assets according to the International Token Classification (ITC) framework. He was heavily involved in the creation of the world’s largest token database for classification and identification data on tokens (TOKENBASE). Maximilian also did heavy academic research in close consultation with Prof. Dr. Philipp Sandner. You can contact Maximilian via e-mail at maximilian.bruckner@21e6.io to request more information on 21e6 Capital AG or ask any questions regarding this article. You can also follow Maximilian on LinkedIn to stay up to date.