ARE STABLECOINS TAKING OVER ETHEREUM?

By: Alvaro Feito Boirac, XBTO Group

USD stablecoins have historically been largely secured over the Ethereum blockchain.

As we enter 2022, this is still the case, although many competing blockchains (both Layer 1 and Layer 2) have started providing increasing utility to these very popular crypto assets. These blockchains are both faster and cheaper.

To paint a clearer picture, we must rewind the clock to Christmas 2018. What was the value of transfers carried out on Ethereum? Looking at stablecoins and ETH, making the area proportional to the value transferred, we see the following:

Most notably, transfers made with ETH were dominating. At slightly less than two percent of this basket, USDT is a minor player. What does it look like today?

Today, ETH has stablecoins biting at the heels. USDC and USDT, previously low volume, now account for 21 percent and 23 percent, respectively. In other words, in December 2021, if you compare the value in USD equivalent of transfers made with DAI, BUSD, PAX, GUSD, USDC, USDT, and ETH, most value is transferred using USD-pegged stablecoins. The USD-pegged tokens above represent 56 percent of the value transferred on Ethereum on a given day in December.

How did we get here?

Compare the evolution of ETH to the leading stablecoin players of this year: USDT, USDC, and DAI. As players in the space, we can appreciate acknowledging a few turning points:

There is no single factor driving this dramatic shift, but the following events had a material impact:

- June 2019: After six months hovering below $7K, bitcoin headed for $10K. Many investors cashed out using Tether (USDT) and began transacting in and out of exchanges. In particular, many Asian investors used Binance [1].

- Mid 2019: Tether moves en masse to Ethereum, partly spurred by Binance shutting down USDT on Omni (The Bitcoin network) in favor of USDT on Ethereum. This growth temporarily clogs Ethereum.

- March 2020: MakerDAO accepts USDC as collateral, adding more stablecoins in the following months.

- Summer 2020: The Total Value Locked (TVL) on DeFi protocols increases exponentially.

- Late 2020: The rising ETH price draws investors, and the transfers related to the trading increase the value Ethereum.

- Early 2021: Tether starts losing dominance in the face of lawsuits from U.S. regulators and questions about its reserves.

- Late 2021: Circle (USDC) establishes itself as a strong Tether competitor through partnerships with Paypal and VISA while playing well with regulators.

- Late 2021: ETH regains dominance as its price surges following EIP-1559, and the crypto bull market continues.

Who is using stablecoins, and for what?

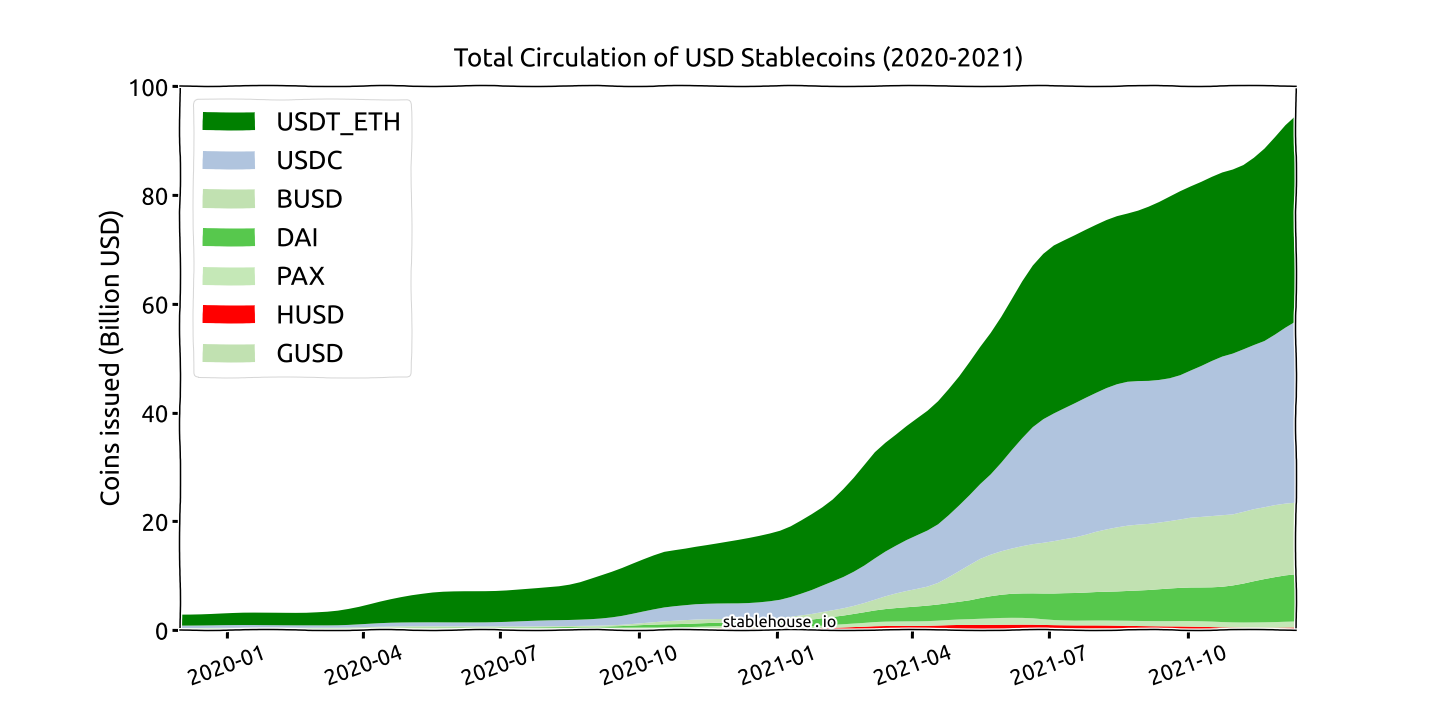

We outline the total value of USD stablecoins circulating on Ethereum in the last two years below:

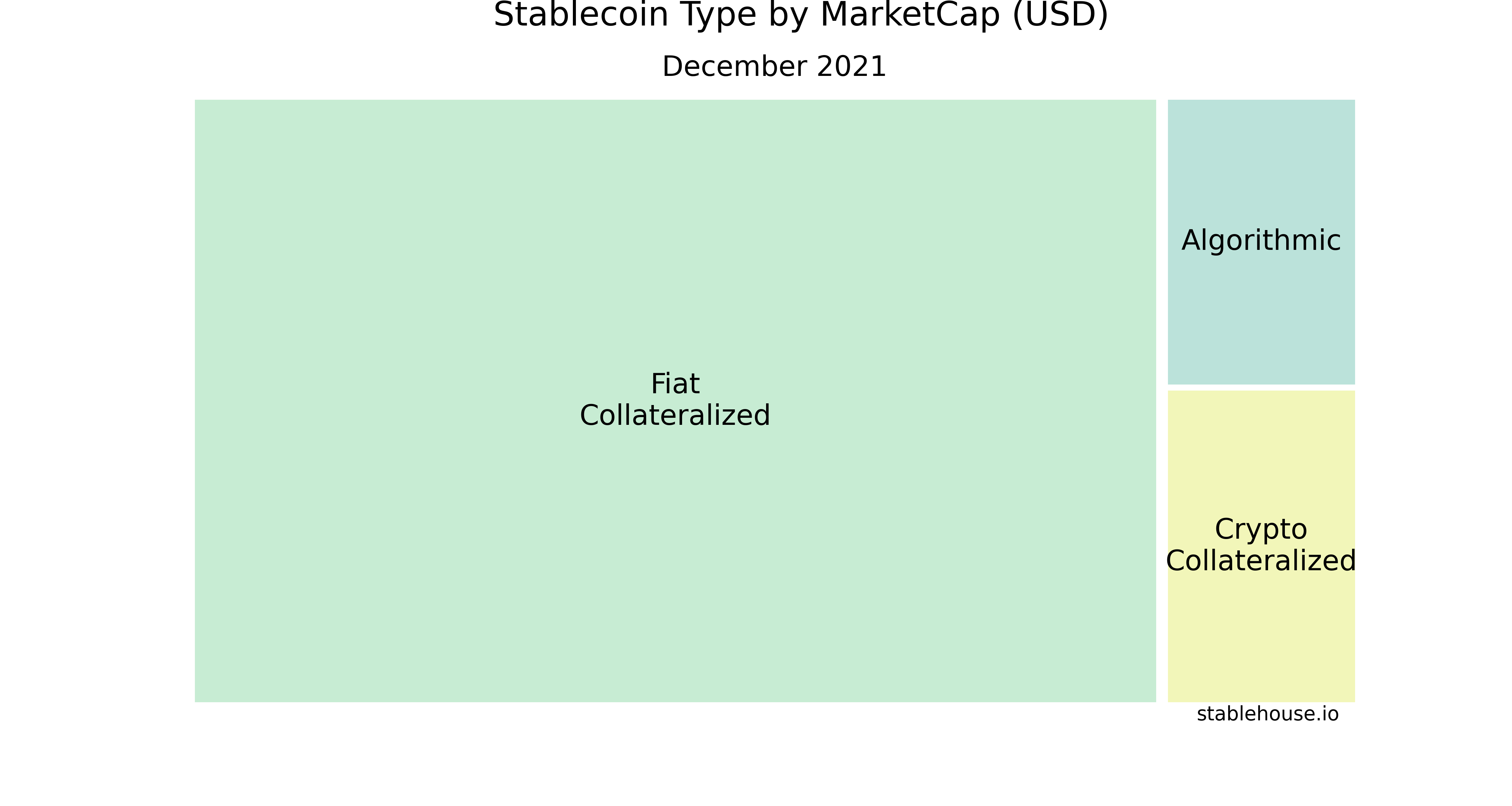

Since January 2020, the market cap of stablecoins issued on Ethereum has grown 31X, from $3B to $95B. More broadly, by mid-December 2021, stablecoins reached a market cap of $160B. If we consider the top 99.6 percent of stablecoins by market cap, this is what their distribution looks like:

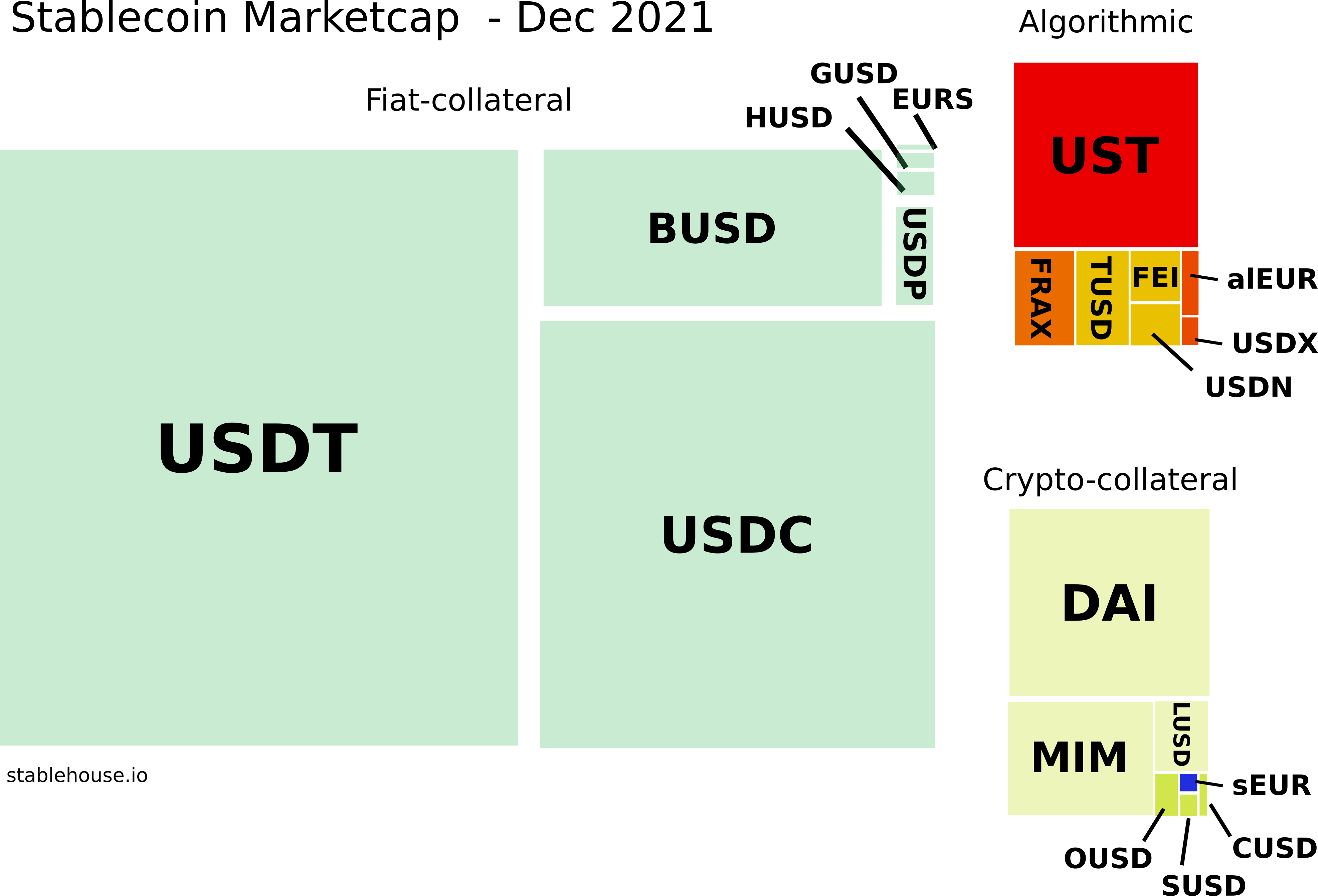

Eighty-three percent of the market cap is fiat-collateralized, and ninety-nine percent of those are U.S. dollar-based. Another nine percent is crypto-collateralized with a final eight percent in the form of algorithmic stablecoins. The graph above can be broken down again into its components, making area proportional to market cap in December 2021:

Let us focus on the leading players: The top three U.S. dollar-based Ethereum stablecoins: USDT, USDC, and DAI.

- They currently facilitate $13B/day (Paypal only averages about $3B/day).

- However, they carry out 200K transactions/day (Paypal carries out 34 million transactions/day)

The data underscores that consumer payments are not a primary use of stablecoins. Instead, their main use is trading and transfers. Indeed, taking the transaction values above, the average transaction is $65K.

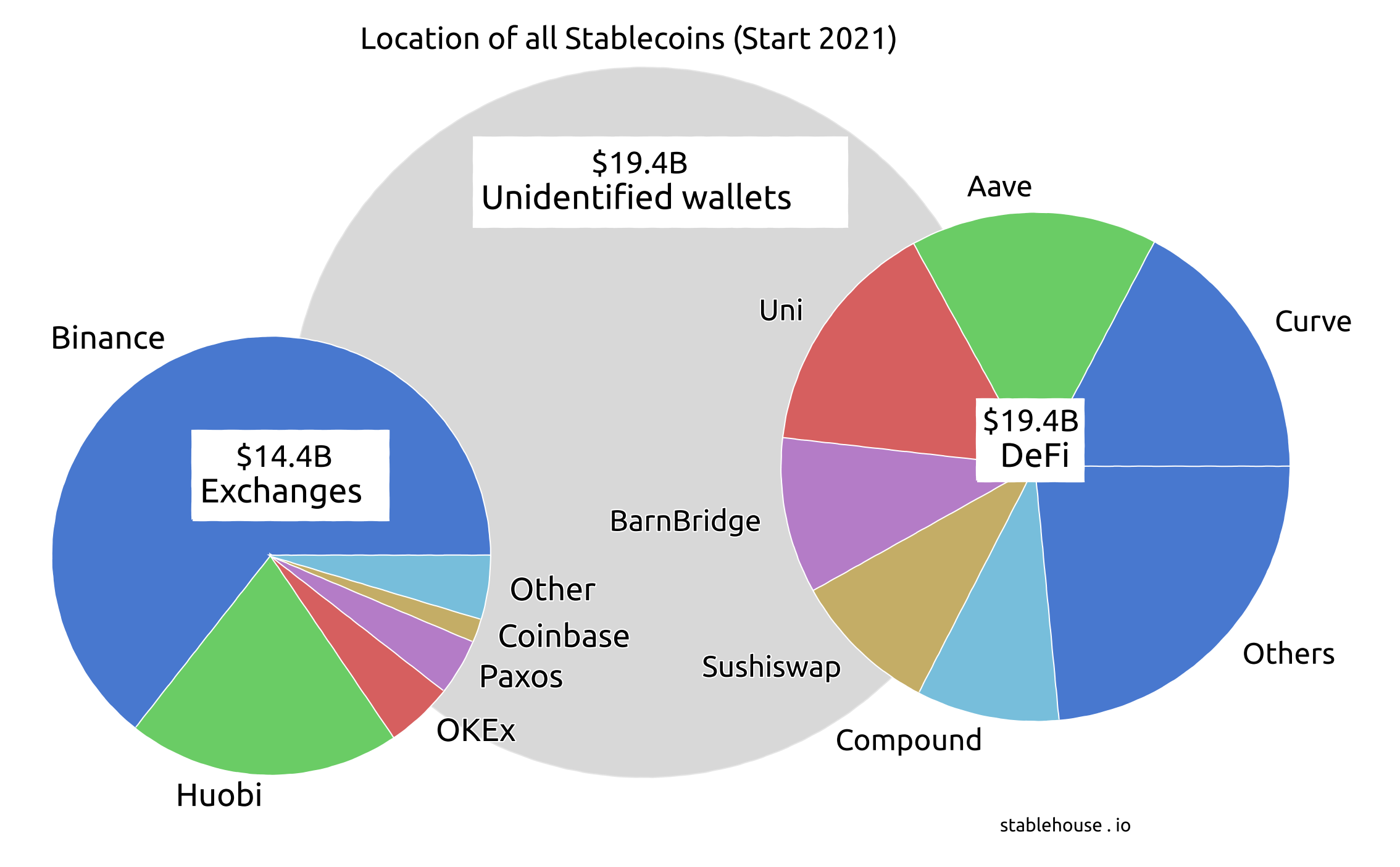

But how are these coins being used? Let us compare to where coins were located last year (January 2021):

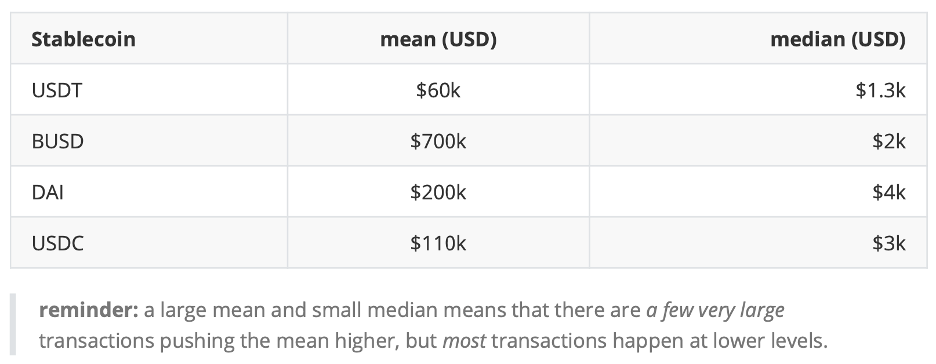

About $34B was in CeFi and DeFi. This metric likely underestimates the actual value, as many of the wallets containing the remaining $19.4B may have been secondary exchange wallets not identified by Nansen's algorithms. One major player stands out: Binance. Last year, Binance's wallets held 64 percent of all stablecoins in exchanges. An obvious interpretation is that traders are using stablecoins as on/off ramps into Binance and as a way to lock in gains. The other large users are exchanges themselves. A clue about stablecoin use is in the average transaction value. Let us look at the mean and median transaction size for the main stablecoins in December 2021.

For BUSD, there are transactions higher than $1M bringing the mean to $700K, but most transactions are closer to $2K. This table tells us that traders, whales, and small traders use stablecoins. BUSD has a very high mean, likely from Binance moving funds around, yet many small transactions dominate the median, showing that small Binance traders are active BUSD users. DAI is interesting because the whales transferring it are more modest, but the median transaction is already $4K. Tether and Circle coins are generally responsible for smaller transactions but still show that institutions and exchanges use them.

The ETH - USD showdown

Stablecoins are used for spot trading and derivatives trading to lock profits, and inter-exchange arbitrage. In addition, more and more options exist to earn a yield on stablecoins. These numbers paint a picture of high growth for stablecoins. But is this positive for Ethereum and its native currency?

There is no question that stablecoins have helped bring new users and traders to Ethereum. However, this sudden influx is also testing the limits of the blockchain. Transaction fees are high, and players are scrambling to find cheaper and faster solutions (be it layer-2 solutions or alternative blockchains such as Tron, Solana, Avalanche, or Binance Chain with their versions of USDT, USDC, BUSD, or DAI).

Finally, if USDT and its close followers become the de facto currency on Ethereum, what is the role of ETH other than paying transaction fees? A valuable ETH is paramount to the security of Ethereum. The miners (or stakers) keep the blockchain secure in exchange for ETH payments. The network must achieve a healthy balance between the demand and use of stablecoins and the native currency.

In conclusion, decentralized systems are influenced by user demands for new products, as shown by the rise of stablecoins and the increased adoption of DeFi. It’s also clear that the rise of new digital asset solutions causes their slew of unforeseen challenges. Additionally, even considering future regulation, the data implies it’s safe to say that stablecoins and DeFi are here to stay, in some way, shape, or form.

Sources

Data Sources: coinmetrics.io | theblock | nansen.ai | duneanalytics | CoinmarketCap

[1] The rise of stablecoins video - The Block

[2] Tether 2019 migration from Omni to Ethereum

[3] Rise of stablecoins PPT - The Block

[4] Statista, Paypal quarterly transfer volume